Weeks ahead of the G7 summit under French presidency, the Iranian dossier is back on the agenda of European foreign ministries through its usual points: diplomacy, nuclear issues, sanctions, and regional security. As it has for two decades, it will be addressed without any multilateral institution having first consolidated its financial toll. Yet the Israeli-American war against the Islamic Republic of Iran and the following blockade of the Strait of Hormuz have thrust into the spotlight a ledger that European capitals have, for twenty years, preferred to keep fragmented: the economic cost that the Islamic Republic imposes on the European Union. What the 2026 sequence revealed in just a few weeks, analysis had already established as a structural reality since the early 2000s.

The European bill extends beyond direct costs. It includes opportunity costs, insurance costs, compliance costs, and social absorption costs. The absence of an aggregated financial assessment weighs heavily. As long as the costs induced by the Islamic Republic are treated as scattered national expenses, they remain outside the European conversation. Yet once they are tallied, the order of magnitude shifts the entire perception of the dossier. Then, the Iranian issue reveals itself for what it has become: a politico-economic dossier with diplomatic ramifications. The 2026’s sequence accelerated this shift, it did not create it.

First point : bank evasion

In August 2024, a UK-registered entity named Zedcex was designated by U.S. authorities, who determined that this single platform had processed over $94 billion in transactions linked to sanctioned Iranian entities during its operation[1]. Zedcex is the visible expression of an invisible architecture composed of hundreds of intermediaries operating within or from the jurisdictions of the European Economic Area, post-Brexit UK, and their immediate partners in the Gulf and Asia.

In practice, the European financial system serves as a central node in Iran’s evasion of Western sanctions. This integration imposes two measurable costs on Europe. The first is the compliance cost, handled by European banks and commercial operators forced to implement enhanced due diligence, filtering procedures, and dedicated teams. The second consists of fines imposed by U.S. authorities for violations of Iran-related sanctions: over the past decade, four major European banks have cumulatively paid more than €12 billion for such breaches[2]. These sums leave the European financial system and never return to the European economy. They represent a net fiscal externality, one that has never been consolidated as such in the annual reports of the banks involved or in the balance sheets of European regulators.

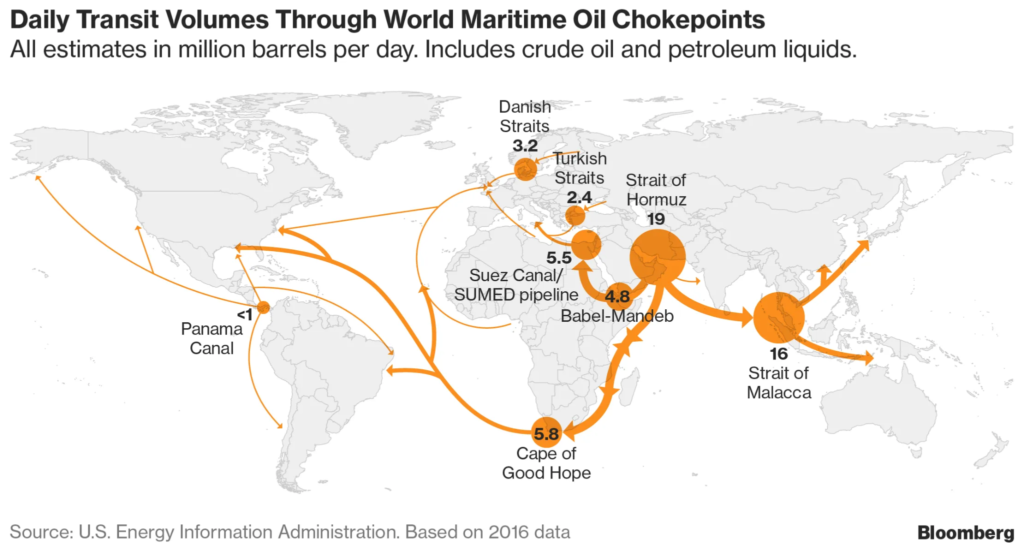

Second point : The maritime inlets : Ormuz, Bab-el-Mandeb, permanent prime

The Strait of Hormuz sees 21 million barrels of oil transit daily, accounting for 30% of global seaborne crude trade and 25% of liquefied natural gas[3]. At the other end of the Arabian Peninsula, the Bab el-Mandeb Strait handles a comparable share of container traffic between Asia and Europe. Since 2024, the campaign led by Yemen’s Houthis, whose arming and training by Iran’s Islamic Revolutionary Guard Corps have been documented by multiple Western analytical centers[4], has forced European shipping companies to reroute a substantial portion of their cargo via the Cape of Good Hope. This detour adds 10 to 14 days to Asia-Europe routes and increases freight costs by roughly 30% on this axis[5].

The simultaneous activation of Hormuz and Bab el-Mandeb during the June 2026 Iran War elevated these costs to a new and lasting level. Brent crude surpassed $100 per barrel, Dutch TTF gas prices doubled to exceed €60 per megawatt-hour by mid-March 2026, the European Central Bank delayed its interest rate cut forecasts, and raised its inflation projection for the year by over one percentage point[6].

Beyond the acute phase, the mere demonstration that dual maritime disruption is now operational has introduced a permanent risk premium into all maritime contracts tied to the region. This premium disproportionately weighs on European operators, who are more exposed than their American or Asian counterparts on these critical trade routes.

Third point : Military asymmetry : a $50 000 drone and a million-dollar interceptor

The growing integration of the Islamic Republic into the trilateral axis with Russia and China has, between 2022 and 2026, produced one of the most revealing economic-military asymmetries of contemporary conflict. A Shahed-136 drone, manufactured in Iran and supplied to Russia for use against Ukrainian targets, costs approximately $50,000 per unit[7]. The Patriot missile required to intercept it over Odesa costs just over $1 million[8]. The asymmetry is a factor of twenty.

The scale of this asymmetry extends far beyond the technical dimension. It means that every Patriot or IRIS-T battery deployed by European democracies for missions tied to Iran’s posture in the Gulf and its allies is a battery unavailable for defense on other fronts. Furthermore, every Iranian drone intercepted consumes twenty times its own value in Western munitions. This structural asymmetry accounts for a significant portion of the rise in European military spending. In 2024, European NATO members collectively spent $454 billion on defense, and Europe as a whole saw its military expenditures increase by 27% in that single year, the sharpest regional rise since the end of the Cold War[9].

Fourth point : State drug : 60% of European heroin, and what remains of Captagon after the Assad’s fall

On July 1st, 2020, Italian customs officers seized a shipment at the port of Salerno containing 84 million Captagon tablets hidden inside rolls of industrial paper. The market value of this seizure exceeded €1 billion, making it, at the time, the largest synthetic drug bust ever recorded in Europe[10]. The cargo’s origin was traced to Syrian facilities controlled since 2014 by Iran’s Islamic Revolutionary Guard Corps (IRGC) and their Lebanese Hezbollah partners. 60% of Afghan heroin and morphine destined for the European market transits through Iranian territory[11]. This route, operated by the IRGC and their criminal affiliates, functions independently of Syria’s political situation. It persists, and will continue to do so, as long as the Iranian regime which maintains control remains in place.

The Captagon production infrastructure, however, underwent a notable geographic shift in 2024–2025 without disappearing, as the fall of the Assad regime might have suggested. Syria’s transitional government systematically dismantled production facilities embedded in military bases, such as those of the 4th Armored Division and its allies. In the months following Assad’s collapse, authorities seized over 200 million tablets, twenty times the volume confiscated by Assad’s forces throughout all of 2024[12]. Yet production simply relocated. In Sudan, plunged into the civil war since 2023, new facilities emerged under the control of criminal actors aligned with the former Syrian regime. In February 2025, Sudanese authorities dismantled a plant in northern Khartoum capable of producing 100,000 tablets per hour. Libya, another institutional void, now hosts new facilities, as documented in a June 2025 UN report[13]. The conclusion is clear: Captagon’s infrastructure survived Syria’s collapse because its surviving architects retained industrial expertise, logistical networks, and commercial outlets. The European market, the second-largest after the Gulf, continues to face sustained supply pressure through alternative routes.

Over the past decade, the aggregated European cost of drug flows tied to Iran’s ecosystem (opioids via the Iranian route, reconfigured Captagon, and Hezbollah-linked money laundering operations) has reached an estimated €100 billion or more in public health, security, and judicial expenses. The post-Assad fragmentation has merely redistributed these costs across new jurisdictions and channels. And with Iran’s regime militarily weakened but structurally intact, any realistic strategic assessment must anticipate its increased reliance on illicit revenues to offset the loss of other income streams.

Fifth point : Regional destabilization and impending migratory pressure

This topic requires an important clarification: migratory flows that the Islamic Republic has helped generate are not, in this analysis, a cost to be attributed to the individuals who compose them. The costs of reception borne by European public budgets over the past three decades are the results from the strategic choices of the Iranian regime. Their cessation depends on the political transformation of the forces driving them. Any restriction on reception would amount to shifting the burden onto the victims themselves.

The military, political, and economic support provided by the Islamic Republic to Bashar al-Assad’s regime between 2011 and 2024 was one of the primary drivers of the Syrian war, which resulted in over 500,000 deaths and 12 million displaced people[14]. Europe absorbed more than 1 million Syrian refugees, with Germany bearing the largest share. The cumulative costs of reception and integration, aggregated by national statistical agencies[15], reached tens of billions of euros per year at the height of the crisis. The European Commission allocated over €60 billion in humanitarian aid to Syria during this period[16]. The collapse of Lebanon, shaped by Hezbollah’s de facto control over the state, produced a second wave that European capitals are again financing, both directly through reconstruction appeals and indirectly through migration management.

Beyond this already absorbed burden, the heaviest migration bill lies ahead of Europe and it is Iranian. The Islamic Republic has a population of 90 million, four times Syria’s pre-war population. The regime’s economic collapse, marked by the unprecedented depreciation of the rial, double-digit inflation since 2018, and an unemployment rate among educated youth estimated between 25 and 40%, has driven mass emigration of skilled individuals to North America and Europe for fifteen years[17]. A prolonged deterioration of Iran’s political and economic situation, assuming a weakened but structurally intact Islamic Republic, would mechanically accelerate this pressure. The potential cost for Europe would no longer be measured in tens, but in hundreds of billions of euros over a decade. Behind the costs already borne looms the bill that European capitals will pay if the Iranian situation worsens without having been anticipated.

Sixth point : Infiltration : eight European services, one diagnosis

Between 2023 and 2026, eight European intelligence agencies published converging reports on the activities of the Islamic Republic of Iran within the European Union and the United Kingdom[18]. This convergence documents five distinct mechanisms operated from Tehran: transnational repression against Iranian dissidents in exile, intelligence gathering targeting European institutions, political influence through associative and academic proxies, cyber operations attributed to groups linked to the Islamic Revolutionary Guard Corps (IRGC), and the use of criminal intermediaries for covert operations.

To date, the defensive costs imposed on European institutions by these activities have not been subject to any public budgetary consolidation. A cautious estimate, based on national intelligence budgets, counterterrorism measures, Europe-wide cyberdefense expenditures[19], and the costs of protecting threatened individuals, places this annual burden at a minimum of several billion euros. The EU’s designation of the IRGC as a terrorist entity has stabilized certain responses without translating them into aggregated accounting.

Addition and order of magnitude

The aggregation of the six categories outlined here, along with secondary dimensions not detailed due to space constraints (such as the unused sectoral capture of European industries through the energy resource option, unaccounted technology transfers via academic cooperation prior to Iran’s March 2019 decree) yields an order of magnitude whose exact precision will remain uncertain until a European institution undertakes a comprehensive consolidation exercise. However, this order of magnitude, based on public sources and the six primary cost lines, is measured in tens of billions of euros per year, most likely at the upper end of that range.

A recent study, using an entirely independent methodological approach, arrives at a convergent estimate. According to its models, the annual economic gain for Europe from a political transformation in Iran would range between €54 billion and €120 billion, depending on the hypothesis about productivity and trade reintegration[20].

At the G7 summit under French presidency, Iran will appear on the agenda as a foreign policy, non-proliferation, and regional security issue. This analysis proposes adding it as a European budgetary concern. As long as the economic costs imposed by the Islamic Republic remain fragmented across separate budgets, they will elude European decision-making. Once consolidated into a single bill, the issue enters a different arbitration universe, where the opportunity cost of inaction becomes measurable and comparable. European diplomatic mediators are made in the language of cost, and it is in this language that the Iranian dossier must now be examined.

Notes

1. Office of Foreign Assets Control (OFAC), U.S. Department of the Treasury, désignation Zedcex Ltd, août 2024. Enquêtes complémentaires : Financial Times, Reuters, 2024.

2. Amendes cumulées BNP Paribas, Standard Chartered, ING et Société Générale au titre des violations des sanctions Iran, 2014-2024. Sources : décisions OFAC, FinCEN et Department of Justice américain.

3. U.S. Energy Information Administration, World Oil Transit Chokepoints, données 2024.

4. International Institute for Strategic Studies, Strategic Survey 2024-2025 ; Atlantic Council, études sur les transferts technologiques Iran-Houthis.

5. Drewry Shipping Consultants, World Container Index hebdomadaire ; Lloyd’s of London, indicateurs des primes maritimes 2024-2026.

6. Banque centrale européenne, Economic Bulletin, printemps 2026.

7. Estimations IISS et Royal United Services Institute, programmes drones iraniens, 2023-2025.

8. Données publiques du Département de la Défense des États-Unis, programme Patriot PAC-3, contrats 2023-2025.

9. Stockholm International Peace Research Institute (SIPRI), Trends in World Military Expenditure 2024, avril 2025.

10. Guardia di Finanza italienne, communication de presse, 1er juillet 2020 ; Center for the Study of Captagon (New Lines Institute), analyse de cas Salerne.

11. Office des Nations Unies contre la drogue et le crime (UNODC), World Drug Report, éditions successives 2018 à 2024.

12. Ministère de l’Intérieur du gouvernement caretaker syrien, communiqués des saisies, premier semestre 2025 ; Stimson Center, Assad’s Fall and Syria’s Fragmented Captagon Industry, 2025.

13. Combating Terrorism Center at West Point, The Future of the Illicit Captagon Drug Trade ; New Lines Institute, Sudan’s Emergence as a New Captagon Hub ; rapport du Panel d’experts des Nations Unies sur la Libye, juin 2025.

14. Haut-Commissariat des Nations Unies pour les Réfugiés (UNHCR) ; Syrian Center for Statistics and Research ; Violations Documentation Center.

15. BAMF (Bundesamt für Migration und Flüchtlinge, Allemagne) ; DGEF (Direction générale des étrangers en France) ; Migrationsverket (Suède), rapports annuels 2015-2024.

16. Commission européenne, Direction générale de la protection civile et des opérations d’aide humanitaire européennes (ECHO), bilans pluriannuels Syrie 2012-2024.

17. Banque mondiale, indicateurs macroéconomiques Iran ; estimations de l’OIT sur le chômage des jeunes ; études sur la diaspora iranienne qualifiée (European University Institute, Migration Policy Institute).

18. France 2050, La menace iranienne en France et en Europe, octobre 2025 ; Bundesamt für Verfassungsschutz (Allemagne), rapports 2023-2024 ; Intelligence and Security Committee (Royaume-Uni), Iran, juillet 2025 ; Bundesamt für Verfassungsschutz und Terrorismusbekämpfung (Autriche), rapport 2024 ; Säkerhetspolisen (Suède), enquête Foxtrot ; Sûreté de l’État (Belgique), communications 2023-2025 ; AIVD (Pays-Bas), rapports annuels 2023-2025 ; Bayerisches Landesamt für Verfassungsschutz, rapport 2024.

19. Agence de l’Union européenne pour la cybersécurité (ENISA), rapports annuels sur les menaces cyber, 2023-2026.

20. Mahdi Ghodsi et Gabriel Felbermayr, Costs of Iran’s Sanctions and Benefits of Sanctions Removal, étude commandée par l’INSM, publiée par le Wiener Institut für Internationale Wirtschaftsvergleiche (wiiw) et le Wirtschaftsforschungsinstitut (WIFO), mars 2026.