Introduction

Iraq is undergoing a highly complex political and economic phase as the parliamentary elections scheduled for November 2025 approach. While the elections represent a pivotal juncture in reshaping the political landscape, the deteriorating economic conditions cast a heavy shadow on voters’ choices and the positions of political forces. Studying the relationship between the economy and elections in Iraq requires a dual approach: the first relates to macroeconomic analysis (economic growth, public budget, stagflation, poverty, and unemployment), while the second is linked to political economy, which encompasses conflicts of interest, elite behavior, and the interaction of external and internal factors. Added to this is the prevailing institutional distrust, a dynamic that will prove decisive in shaping electoral behavior as well as political and economic stability in Iraq.

1. The Current Economic Landscape

1.1 Economic Growth and Rentierism

Data indicate a sharp decline in economic growth, reaching about –2.9% in 2024, compared to 0.5% in 2023 and 8% in 2022, due to structural imbalances and the weakness of productive sectors. Oil accounts for more than 90% of public revenues and over 99% of total exports. This rentier structure makes the Iraqi state hostage to global oil price fluctuations, whereby any drop in prices immediately translates into a fiscal crisis. This recurring pattern is temporarily alleviated whenever international oil prices recover, creating only short-lived periods of fiscal relief.

1.2 Public Budget and Uncontrolled Spending

Despite the approval of the three-year budget (2023–2025), the phenomenon of off-budget spending remains a major challenge, undermining transparency and creating unaccounted-for financial commitments, thus weakening fiscal stability. The table below shows the magnitude of off-budget spending during 2015–2023, based on reports from the Federal Board of Supreme Audit and official statements:

Table 1. Off-Budget Revenues and Expenditures (Trillion IQD)

| Year | Special Funds | Unremitted Ministerial Revenues | Emergency Expenditures | Total |

| 2015 | 1,150 | 1,800 | 2,700 | 5,650 |

| 2017 | 900 | 2,000 | 1,900 | 4,800 |

| 2019 | 1,000 | 2,500 | 1,200 | 4,700 |

| 2022 | 1,400 | 2,800 | 800 | 5,000 |

| 2023 | 1,200 | 2,600 | 600 | 4,400 |

| Total | – | – | – | 24,550 |

Source: Analytical estimates based on reports from the Ministry of Finance, the Federal Board of Supreme Audit and official statements.

Off-budget spending amounted to about (24.55) trillion IQD between (2015–2023) . This practice is not an exceptional occurrence but rather a recurrent pattern that has fostered a non-transparent fiscal environment, weakened the state’s ability to implement sound fiscal policies, distorted deficit and surplus figures, and obstructed genuine development planning. and contributed to higher public expenditures. Consequently, domestic public debt rose to about (92) trillion IQD by Q3 2025, equivalent to more than (25%) of GDP.

Wages and salaries alone consume over (60%) of total government expenditure (about 90 trillion IQD annually), posing recurrent challenges in securing monthly payments, which depend primarily on oil revenues. When oil revenues fall short, the government resorts to domestic borrowing.

1.3 Inflation and Living Standards

Between (2022–2024), Iraq witnessed inflationary waves driven by rising food and energy prices and occasional depreciation of the Iraqi dinar against the U.S. dollar. This hurt citizens’ purchasing power, leading to an increase in poverty levels affecting more than 25% of the population. By mid-2025, however, inflation had dropped sharply, even turning negative in June (–0.6%), which triggered a deep recession in local markets. A key factor behind this was Iraq’s heavy reliance on imports from Iran(over 400 goods and services, worth around USD 7 billion annually) which were disrupted due to the Iranian–Israeli war.

1.4 Unemployment and Labor Market

Youth unemployment exceeds 40%, while around 60% of the labor force is engaged in the informal economy, limiting the government’s ability to absorb social pressures.

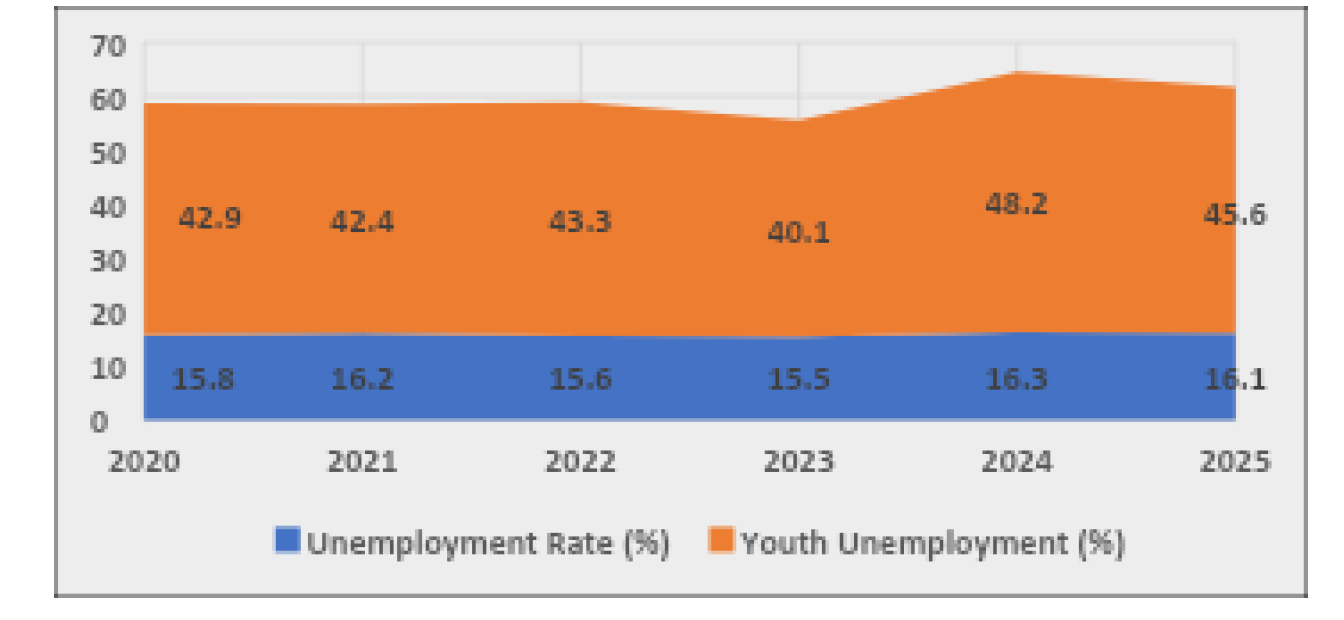

Figure – 1 – Unemployment Rates in Iraq (2020–2025)

Source: Iraqi Ministry of Planning, Central Statistical Organization, Annual Statistical Reports (2020–2025).

Youth unemployment rose from 42.9% in 2020 to 48.2% in 2024, driving up overall unemployment to 16.3% (Figure 1) Iraq has entered a demographic window (a predominantly young society) that requires micro and small-scale projects, especially for youth. Yet, institutional support is weak, and access to credit is hindered by complex procedures.

1.5 The Financial and Banking System

The banking sector has suffered from sanctions and restrictions on dollar access, particularly after 2023, when more than (40) private banks were barred from participating in the foreign currency auction due to alleged corruption and terror financing (as stated by the U.S. Treasury). Over (85%) of the money supply remains outside the banking system. By June 2025, currency in circulation amounted to (98.3) trillion IQD, of which (90.9) trillion was held outside banks and only (7.4) trillion within the banking sector. This reflects a lack of trust in the financial system and weak financial inclusion, undermining the effectiveness of monetary policy.

2- The Economic Impact on Electoral Behavior

A- Punitive Voting

This is a well-established phenomenon in political economy literature, where voters hold the government accountable for economic deterioration even if caused by external factors (such as oil prices or global crises).

In Iraq, however, following the October 2019 protests and the subsequent political deadlock, a new electoral awareness emerged among youth and civil groups. They tend to punish dominant forces either by boycotting elections or voting for emerging independent movements. This was clearly demonstrated in the 2021 elections through the low turnout (around 41%) and the rise of new forces (such as Imtidad and Eshraqat Kanoon) at the expense of traditional blocs.

The 2025 elections are likely to repeat this pattern, especially if the deterioration of the dinar exchange rate, rising inflation, and poor public services persist. The expected outcome is that large parties will face relative losses, while independents or opposition coalitions may achieve symbolic but influential gains in the post-election landscape.

B- Political Apathy

There is a close relationship between economic decline and “political apathy,” as voters perceive participation as pointless if their living conditions do not improve.

In Iraq, youth make up more than 60% of the population, yet they face high unemployment (exceeding 25%) and limited opportunities for productive jobs outside the public sector. Iraqis compare their income and prospects with their Gulf counterparts (where per capita income is almost ten times higher). This gap deepens the sense of distrust in political institutions and often translates into electoral disengagement.

The effects of this mindset are reflected in lower participation rates in 2025 (potentially dropping below 2021 levels if no tangible reforms occur). Moreover, since participation remains concentrated in traditional partisan bases (Shiite, Sunni, Kurdish), the chances for real change through the ballot box are weakened.

C- Populism Trend

Economic crises often push candidates to adopt populist rhetoric: immediate and easily marketable promises, but difficult to implement, designed to mobilize angry voters. Accordingly, campaign slogans in the 2025 elections are expected to focus on:

- Increasing salaries and public-sector employment (despite the inflated bureaucracy that already consumes over 70% of the budget).

- Subsidizing food and fuel (while Iraq faces IMF and financial institutions’ pressure to reduce subsidies).

- Expanding the social welfare network (despite limited and volatile oil revenues).

These promises appease discontented voters but later prove difficult to fulfill, worsening the trust gap between voters and politicians. This may help some blocs secure short-term electoral gains but will place the state in a post-election fiscal dilemma, further undermining the economic and political system.

3- The Economy as a Tool of Political Struggle

In Iraq, the economy has evolved from merely reflecting the general political climate to becoming an active instrument used by political actors to consolidate power or undermine rivals. This dynamic is visible across several dimensions. At the core are patronage networks, whereby governments deploy public funds and economic resources to secure electoral loyalty. Dominant parties exploit ministerial and institutional positions, awarding public-sector jobs or government contracts to supporters. Over successive election cycles, these networks expand, transforming the economy from a tool of development into a mechanism for political allegiance. This entrenchment contributes to a “political rentier economy,” where oil revenues are converted into electoral gains rather than invested in productive projects, embedding structural challenges that persist across political administrations.

Opposition forces also manipulate economic conditions to their advantage. Periods of crisis—manifested in rising unemployment, inflation, currency devaluation, and weak public services—serve as evidence of the ruling parties’ mismanagement. A notable example is the discourse following the 2019 protests, when emerging political blocs linked economic dysfunction directly to corruption. While this strategy strengthens the opposition’s narrative, it often stops short of offering viable solutions, rendering economic grievances primarily a tool of political competition rather than a platform for reform.

External actors further complicate Iraq’s economic and political landscape. Economic instruments such as oil, financial transfers, and trade have become avenues for foreign influence. The U.S. Federal Reserve, for instance, exerts leverage through control over dollar transfers, while Turkey uses energy exports via the Ceyhan pipeline to influence both Baghdad and Erbil. In this context, the economy functions as a conduit for regional and international power struggles, amplifying political competition while undermining sustainable development.

4- The Regional and International Dimension

Iraqi elections do not occur in a domestic vacuum; they are profoundly shaped by international and regional dynamics, reflecting the country’s power-sharing political system and the interconnection of its economy with neighboring states. The United States, for instance, employs financial instruments as a means of influence. Through mechanisms such as the Office of Foreign Assets Control (OFAC), it monitors financial transfers and restricts the flow of U.S. dollars to black markets or armed groups. U.S. oversight of Iraqi banks has directly impacted the dinar exchange rate in 2023–2024. These measures aim to prevent the diversion of oil and dollars to regional adversaries, particularly Iran, thereby shaping Iraq’s internal balance of political power.

Iran wields influence through deep economic ties with Iraq, rooted in both geographic proximity and ideological alignment. Annual trade flows exceed 11 billion USD, encompassing imports of gas, electricity, and over 400 goods and services for the private sector. These connections allow Iran to exercise leverage over the Iraqi government and political parties, supporting allies or exerting pressure by adjusting or withholding supplies. The strategic goal is to maintain political influence and secure the continued presence of its partners in parliament.

Gulf states and Turkey also seek to shape Iraq’s political and economic landscape. Gulf countries primarily use investments in energy and infrastructure to strengthen influence, exemplified by electricity interconnection projects with Saudi Arabia and other Gulf nations. Turkey leverages control over water resources, trade, and oil exports, particularly through the Ceyhan pipeline, providing it with a strategic bargaining position over Baghdad and Erbil. With trade volumes exceeding 20 billion USD, Turkey remains a crucial economic actor, reinforcing its regional influence over Iraq and the Kurdistan Region.

5- Possible Scenarios in the Context of the 2025 Parliamentary Elections

In this paragraph, the author presents his own hypothesis regarding potential scenarios in the context of the 2025 elections. All information and data are based on his independent analysis.

Scenario One: Relative Stability

This scenario assumes that oil prices remain above 80 USD per barrel, providing sufficient revenues for the Iraqi budget, while financial management shows relative improvement through controlled expenditures, reduced waste, and a stabilized exchange rate. Security and political conditions remain adequate to prevent widespread unrest. Under these circumstances, the government can reliably fund salaries and social support without triggering fiscal crises. Foreign currency reserves at the Central Bank strengthen, alleviating pressure on the dinar, and limited infrastructure investments in areas such as roads, electricity, and water become feasible. Politically, ruling parties can present these modest achievements as evidence of competent economic management, reducing the appeal of opposition rhetoric, though not eliminating it entirely. Voter turnout is likely to remain moderate, around 40–45%, with some citizens inclined to give traditional powers another opportunity.

Scenario Two: Prolonged Crisis

In this scenario, Iraq experiences sustained stagflation, with inflation exceeding 10–15%, stagnant local markets, and weak industrial and agricultural activity. Unemployment remains high, particularly among youth and graduates, while government investment spending slows or stalls. Economically, this leads to a tangible erosion of citizens’ purchasing power, rising poverty rates potentially surpassing 30% of the population, and weakened confidence in domestic markets, prompting growth in the informal economy. Politically, opposition groups and independents are likely to gain ground by capitalizing on public dissatisfaction, intensifying punitive voting against ruling parties. Voter turnout among youth may decline, although core party supporters remain cohesive. The resulting parliament could be more fragmented, with an increase in independents and a relative reduction in large blocs.

Scenario Three: Disruption

This scenario envisions a significant external or internal shock, such as oil prices falling below 60 USD per barrel, new financial or economic sanctions imposed by the United States or other international actors, widespread security unrest, or renewed terrorist activity in certain areas, combined with government failure to maintain financial and monetary stability. The economic consequences would include a partial collapse marked by a large fiscal deficit, escalating debt (potentially exceeding 110 trillion IQD or roughly 45% of GDP), a payroll crisis, and sharp dinar depreciation. Popular protests could expand beyond the scale of those in October 2019, and government paralysis might lead to postponed or disrupted elections in some regions. Politically, stable and legitimate elections would be difficult to hold, new protest-driven forces could emerge to reshape the political landscape, and transitional or consensus-based governments under regional or international sponsorship might become necessary.

Conclusion

The Iraqi experience since 2003 confirms that the economy is not a secondary factor in elections but rather a fundamental determinant of the nature and stability of the political system. Analysing the economic indicators for the period 2020–2025 reveals that Iraq is heading toward decisive elections in the midst of a fragile economy suffering from structural imbalances rooted in oil rent dependency. This reliance has been mirrored in an increased dependence on monetary financing, which in turn expanded domestic debt, in addition to a stagflation environment that struck local markets and led to higher youth unemployment. Combined with a shifting public mood, these dynamics could produce electoral outcomes that reshape the balance of power.

From a political economy perspective, the greatest challenge does not lie in managing the elections themselves but in the capacity of Iraq’s political system to articulate a new economic–social contract that ensures a more equitable distribution of resources and restores trust between the state and society. This mixture provides an opportunity for popular protest expressed either through voting or through abstention in the 2025 parliamentary elections. Ultimately, the economic figures and data demonstrate that the primary challenge before the political system is not merely winning elections, but presenting a credible and actionable economic package capable of rebuilding public trust in the state.