Since the second half of the 20th century, despite the initially pivotal role played by pipelines, maritime transports has established itself as the backbone of the global hydrocarbon trade (the success of oil tankers, the development of LNG carriers). In this context, the Strait of Hormuz has taken on capital importance. This strategic passage between the Gulf and international markets handles around 25% of global oil flows and nearly 20% of liquefied natural gas (LNG) flows, amounting to approximately 20 millions barrels of oil and nearly 320 millions m3 of LNG every day.

Long envisaged as a worst-case scenario whose likelihood remained uncertain, the blockage of this strait – following the war launched on the 28 February 2026 by the United States and Israel against Iran – has suddenly become a reality, with serious repercussions for both the supply and prices of hydrocarbons. The pressure exerted by Tehran on this vital sea route has thus highlighted the global energy system’s critical dependence on it.

The prospect of the Strait of Hormuz reopening, following Donald Trump’s announcement of a ceasefire on 7 April 2027, does not, however, resolve the problem, as conditions for navigation in this waterway are likely to be significantly different from those that prevailed before the conflict, particularly if new tensions arise and if Iran demands transit fees. The threat posed by the passage throught these straits to global trade increased further with the Houthis’ entry into the on 28 March 2026. Concerns now also extend to the Strait of Bab el-Mandeb, another strategic chokepoint, linking the Red Sea to the Indian Ocean. The proliferation of threats to these major chokepoints poses a significant risk of disruption to global energy flows and fuels the debate on how hydrocarbons should be transported.

Source : BBC News

Given the vulnerability of maritime transport highlighted by this crisis, pipelines are once again emerging as attractive levers for strategic diversification. In Saudi Arabia, the Gulf States and, to a lesser extent the Middle East, these land-based infrastructures can contribute to a gradual reconfiguration of the energy routes. The aim is not so much to replace maritime routes as to mitigate the risks associated with them by offering credible and secure alternatives. It is worth recalling that, in the 1990s, following the end of the bipolar world, land transport was prioritised, under pressure from Turkey, to transport newly extracted Russian and Azerbaijani gas and oil resources, avoiding, for security reasons, having them pass through the Bosphorus Strait and Istanbul, a megacity of over 15 millions inhabitants.

While in recent decades the maritime transport of hydrocarbons (particularly oil) appeared to have gained the upper hand over pipeline transport – which is more inflexible as it requires long-term contracts and significant infrastructure – the threat now looming over the straits is restoring the relevance of pipelines. In any case, a comparative analysis of these different options using concrete examples, both recent and older, helps to shed light on the dynamics at play, assess the room for manoeuvre available to producer states, and identify the structural constraints weighing on these networks in a particularly unstable international context.

We will therefore first examine how the Gulf producer countries (in particularly Saudi Arabia and the United Arab Emirates) attempted to overcome over the blockage of the Strait of Hormuz (1), before placing this issue within the context of previous experiences of land-based oil transport in the Middle East (2) and drawing lessons from the 2026 crisis for the future transport of oil and gas in the region (3).

Overcoming maritime constraints : the advantages and limitations of alternative land-based energy corridors in the Gulf

This is not the first time that the Strait of Hormuz has been at the center of major geopolitical tensions and has highlighted the structural vulnerability of maritime energy flows. During the Iran-Iraq war (1980-1988), the “Tanker war” saw several hundred attacks by both sides on oil tankers, disturbing crude transit and causing sharp price fluctuations. Subsequently, Iran threatened to close the Strait in 2011-2012, in response to international sanctions imposed on it over the nuclear issue. The period 2019-2020 saw attacks on tankers and missile strikes in the area, notably off the coast of the United Arabs Emirates and in the Sea of Oman, against a backdrop of high tensions between Tehran and Washington that had marked Donald Trump’s first term, following the withdrawal of the JCPoA. Although no lasting disruption was observed at the time, these incidents highlighted the critical dependence of oil-producing states on this waterway and the need to diversify the export routes.

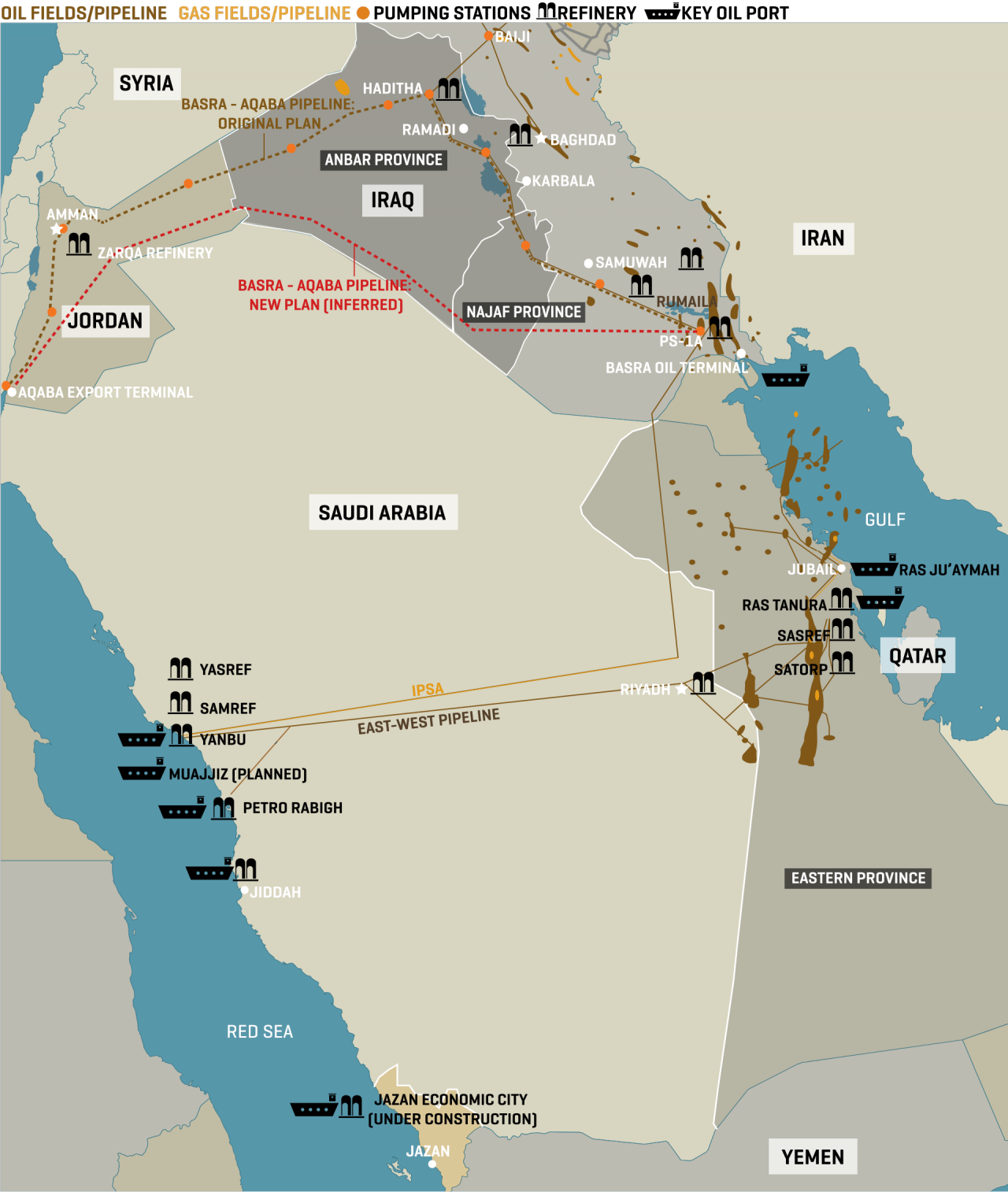

From this perspective, Saudi Arabia appears to be the country that has most systematically developed alternative solutions. As early as the 1980s, during the turmoil in the Persique Gulf caused by the Iran-Iraq War, the Kingdom of Saudi Arabia made substantial investments to link its main eastern oil fields to the Red Sea. This conflict even saw Baghdad cooperate with Ryad to develop l’IPSA (Iraq-Saudi Arabia Pipeline), an oil pipeline that connected its Iraqi oil field in Basra to the Saudi coast of the Red Sea, after crossing the Arabic Peninsula. At the time of the Gulf War, however, this pipeline was blocked by the Saudis, who had in the meantime also developed the East-West pipeline or Petroline. This pipeline runs from Abqaiq to the port of Yanbu, covering a distance of nearly 1,200 kilometers. Its capacity, which stood around 2 millions barrels per day before the 2026 crisis, has been gradually increased to nearly 5 million barrels per day (and could reach 7 million barrels per day). Whereas previously only a third of Saudi oil exports used Petroline, it has now become the only possible route for Saudi oil exports and helps to limit Riyadh’s dependence to the Strait of Hormuz.

Source : MEES

However, due to its long route and its reliance on essential infrastructure such as its pumping stations, the Petroline pipeline is not without its vulnerabilities. Over the decades, it has experienced occasional disruptions linked to the significant tensions that have arisen in the region. The Gulf War (1990-1991) certainly confirmed the value of Petroline in bypassing the Strait of Hormuz. However, although it was not directly hit, the pipeline remained within range of Iraqi SCUD missiles at the same time. This vulnerability was later highlighted in 2019, during a series of drone attacks attributed to the Houthis. In May, in particular, the Houthis claimed responsibility for spectacular strikes against two pumping stations, which disrupted traffic of the pipeline. In the months that followed, further similar attacks targeted oil fields (Abqaiq and Khurais) or facilities near the pipeline, significantly affecting Saudi Arabia’s daily oil production. The war launched against Iran in February 2026 cemented Petroline’s role as an alternative to maritime transit through the Strait of Hormuz and pushed its capacity to the limit. However, Iranian reprisals against Gulf states did not spare Saudi Arabia, targeting its oil facilities (in particular on 2 March 2026, the Ras Tanura refinery) near the pipeline, and even the pipeline itself. The pipeline is therefore a viable alternative, but it is located in an environment that remains dangerous.

The United Arab Emirates followed suit by developing an oil pipeline between the Habshan field and the port of Fujaïrah, located on the Oman Gulf, just beyond the Strait of Hormuz. Stretching some 400km, this energy corridor, also known as the Abu Dhabi pipeline, has a capacity of around 1.5 million barrels per day and is a key instrument in securing Emirati exports. The port of Fujaïrah has, moreover, established itself as a leading energy hub, combining storage, refinery and exports capabilities.

But here too, geopolitical constraints remain. Recurring tensions in the Oman Gulf, particularly during crises involving Iran, have led to temporary disruptions or adjustment to flow rates for security reasons, notably between 2019 and 2022, following attacks on tankers and energy infrastructure carried out by pro-iranians groups and regional militias amid ongoing tensions between Iran and the Gulf States. For example, in May 2019, Habshan-Fujaïrah pipeline had to temporarily reduce its flow following an attack on facilities near Fujaïrah, disrupting exports. During the 2026 war, several Iranian drone attacks targeted the Fujaïrah oil port area, the terminus of the Abu Dhabi pipeline. On 14 March 2026 in particular, fires were observed at its terminal and at two of its pumping stations. These incidents partially disrupted oil shipments. Once again, these events show that the land-based bypass of the strait does not eliminate the geopolitical risk, but merely shifts its term to some extent.

In the context created by the 2026 war against Iran, several international institutions have highlighted the role of land-based energy transport infrastructures as a backup solution in the event of the closure of the Strait of Hormuz. The US Energy Information Administration estimates that the combined capability of Saudi and Emirati pipelines capable of bypassing the strait lies between 2.6 and 4.7 barrels per day, a volume significantly lower than the approximately 20 millions barrels that pass through the strait daily. The International Energy Agency puts forward similar estimates, assessing the capacity that can actually be mobilised at between 3.5 and 5.5 millions barrels per day. These figures reflect a fundamental shift: the desire to reduce dependence on strategic maritime chokepoints by developing land corridors. Nevertheless, these facilities cannot fully replace maritime routes. Their combined capacity remains less than half the volume passing through Hormuz, while maritime transport retains a decisive advantage in terms of volume and flexibility, allowing flows to be rapidly adapted to changes in global demand.

From an economic perspective, however, oil pipelines offer undeniable advantages. Once operational, they ensure a continuous supply at relatively controlled cost, regardless of the uncertainties of maritime transport. They also guarantee greater predictability on supply flows, an essential factor for both producers and importers. These benefits must, however, be balanced against high investment costs, often running into billions of dollars, as well as a heavy reliance on the political stability of the territories through which they pass.

Finally, the issue of security remains central. Unlike maritime traffic, which is dispersed and difficult to disrupt entirely, pipelines are identifiable and vulnerable fixed targets. Sabotages, attacks or drone strikes can quickly disrupt their operation. Saudi facilities, in particular, have experienced this on several occasions, even before the 2026 crisis. Like maritime transport, land corridors have vulnerabilities, even if they are of a different nature.

The reasons behind the decline of overland oil transport routes in the Middle East since the second half of the 20th century

To be fully understood, the current situation in the Gulf regarding oil flows has must be examined in the light of previous experiences with pipelines transport, which have been disrupted or even brought to a standstill by incessant crises in the Middle East.

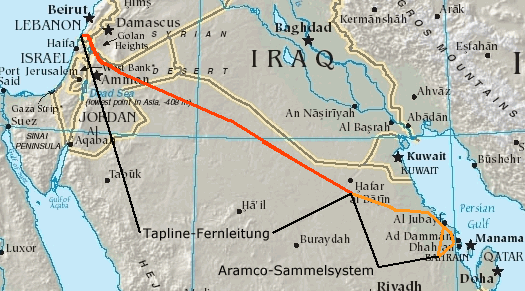

Designed in 1945 following the Quincy Agreement between Roosevelt and Ibn Saoud and commissioned in the early 1950s, the Trans-Arabian pipeline (Tapline) connected the Saudi oil field to the Mediterranean, crossing Jordan, Syria and Lebanon, with a port terminal at Saïda. The objective was clear : to provide direct access to European markets by reducing the cost and lead times of maritime transport. Symbolic of a golden age of pipeline, this oil pipeline exported up to half of Saudi Arabia’s productions. Very early on, however, it proved vulnerable to geopolitical shocks. The Six-Day war in 1967, which enabled Israel to seize the Golan Heights, placed a section of the infrastructure under Israeli control, though it did not interrupt its operation. Palestinian sabotage subsequently damaged it.

Source : Wikipédia

From the late 1970s onwards, the decline of Tapline became virtually irreversible for economic and strategic reasons. In 1976, the Lebanon and Syrians sections of the pipeline were closed due to disagreements between Riyad and Beirut and Damascus over transit fees. From then on, facing fierce competition from the spectacular rise of maritime transport, it supplied only Jordan until the Gulf war dealt the final blow. Saudi Arabia decided to cut off Amman’s oil supply due to Jordan’s support for Saddam Hussein’s Iraq. Since then, attempts to reactivate Tapline have failed. This setback occurred against a regional backdrop profoundly transformed by the Iran-Iraq War (1980-1988). Whilst the “Tanker War” (1984-1988) weakened the Gulf’s maritime routes, it did not, however, benefit the Syrian land corridor. On the contrary, regional actors favoured solutions deemed politically safer, as they bypassed Syrian territory. Moreover, inter-arabe rivalries, particularly between Damascus and Baghdad, contributed to Syria’s long-term exclusion from the major energy routes. This is also illustrated by the suspension of Kirkouk-Banias pipeline.

Before the Second World War, the oil fields of Kirkuk in northern Iraq were linked to the Mediterranean by the Mosul-Haïfa pipeline[1]. Put into service in 1935, this pipeline was a major strategic artery for the United Kingdom in the region. Palestine and Transjordan were then under British mandate, whereas Iraq, although formally independent since 1932, remained in practice under London’s control. The infrastructure was therefore fiercely defended by the British during the Arab revolt of 1936-1939, and then at the start of the Second World War, before being abandoned in 1948, following the First Arab-Israeli War and the creation of the State of Israel, with Haïfa having become an Israeli port. This enabled Syria to host the bulk of the route of a new, more northerly pipeline, intended to transport oil from Kirkuk to the ports of Tripoli and Banias. Opened in 1952, the Kirkuk-Banias pipeline thus constituted a major outlet for Iraqi oil bound for Europe and a strategic asset for Syria, but it was to suffer from the conflict between the two Ba’athist regimes, fuelled by disputes over transit tariffs.

Closed in 1976, this pipeline was reopened and closed again on several occasions. After restoring it in 1978, Syria decided to block it once more in 1982, in order to support Iran in its conflict with Irak, thereby depriving the latter of strategic access to the Mediterranean for the export of its hydrocarbons. The infrastructure remained at a standstill for the entire duration of the Iran-Iraq War and, despite attempts to revive it in the 1990s, it never regained its original role, before being severely damaged by bombing by US forces during their intervention in Iraq in 2003. Since then, the tensions and conflicts in the region have combined to derail numerous revival projects. In April 2025, however, an Iraqi delegation proposed to Ahmed al-Charaa’s new Syrian government that they work towards bringing the equipment back into service…

This appears all the more uncertain given that, as early as 1977, a shift towards an alternative route took place with the commissioning of the Kirkuk–Ceyhan pipeline. Starting in northern Iraq, this pipeline bypasses Syria by passing through Turkey to reach the port of Ceyhan on the Mediterranean. However, although this corridor remains operational, it has been severely affected by successive upheavals in the region. Since the US intervention in Iraq in 2003 and the ensuing destabilisation, it has been the target of regular acts of sabotage, which explains why it is underutilised. Furthermore, the operation of this pipeline is affected by the oil dispute between the Iraqi federal government and the Kurdistan Regional Government. Finally, following an arbitration ruling and an agreement between the two parties, operations on the pipeline in question resumed in September 2025. Interest in this land-based oil transport route has been revived since the closure of the Strait of Hormuz, which has hit Iraq hard. Its role has been reaffirmed once again recently. On 17 March 2026, following negotiations mediated by the US, the authorities in Iraqi Kurdistan authorised the resumption of oil exports via this pipeline, which had been suspended for two weeks following attacks by pro-Iranian militias on oil facilities.

As for Syria, although it is no longer a strategic transit country, it remains involved in plans for overland oil and gas routes in the region. In the early 2000s, a proposed gas pipeline (known as the Gulf-Turkey Gas Pipeline) designed to transport Qatari gas to Europe was planned to pass through Saudi Arabia, Jordan, Syria and Turkey. But in 2009, under pressure from its Russian ally, which was determined to preserve its European gas markets, Damascus refused to allow the pipeline to be built. The Syrian civil war made it impossible to resume the project, and an alternative route, bypassing Syria via Kuwait and an unstable Iraq, was abandoned. Do the new circumstances prevailing in Syria since the fall of the Ba’athist regime in 2024 and the disruptions to shipping in the Strait of Hormuz caused by the 2026 war against Iran offer a new chance for this project to succeed? In any case, this final example illustrates the extent to which land-based pipeline projects for hydrocarbon transport are subject to formidable geopolitical constraints and rigidities. It explains why the flexibility of maritime transport was preferred, particularly from the 1960s and 1970s onwards, following the advent of supertankers.

Nevertheless, memories of the golden age of pipelines in the mid-20th century continue to shape the strategic thinking of the leaders of the countries concerned. Over the last two decades of the 20th century, several projects thus explored the possibility of bringing the Tapline back into service. In a more realistic but no less significant move, the Saudi authorities are now considering proposing its inclusion on the UNESCO World Heritage List, as the kingdom’s first major industrial achievement. Since the fall of the Ba’athist regime in Syria, Iraqi leaders, seeking to diversify their export routes and reduce their dependence on the Gulf, have proposed to their Lebanese and Syrian counterparts that the Kirkuk-Banias-Tripoli oil pipeline be reactivated. The war against Iran in 2026 and the uncertainties surrounding the Strait of Hormuz are reviving the nostalgic dream of restoring the old overland oil corridors of the last century.

Initial lessons from the 2026 crisis for oil and gas transport in the Middle East and the Eastern Mediterranean

The energy crisis triggered by the war against Iran, has already led to one clear conclusion: oil pipelines cannot entirely replace maritime transport. Their primary role is one of security, enabling a minimal level of exports to be maintained in the event of a blockage of strategic maritime routes, without, however, being able to handle the full volume of global trade.

The example of the role played by the Habshan-Fujaïrah oil pipeline, since the start of the 2026 crises is a case in point. Before the crisis, flow through this pipeline stood at around 1 million barrels per day, representing approximately 30% of the total emirati exports (3.4 million barrels per day),two-thirds of which were therefore transported by sea. Following 28 February 2026 and the blockage of the Strait of Hormuz, the Emirates’ exports fell to 1.8 barrels per day, less than half the pre-crisis total, and are now carried exclusively via the Habshan-Fujaïrah pipeline, which is operating at full capacity, while being subject to temporary interruption caused by Iranian attacks. These figures show that the Habshan-Fujaïrah pipeline primarily enables partial and strategic continuity of exports, but does not replace maritime routes. It is a fallback measure but not a substitute solution25.

Maritime transport, therefore, continues to play a central role in delivering the majority of oil to global markets, offering a degree of flexibility and capacity that existing pipelines cannot match. It accounts for around 65% of global oil transit. In the Middle-East, however, the 2026 crisis reinforced the importance of oil pipelines as safety nets, thereby justifying the continuation of a hybrid model combining land corridors and maritime routes. Saudi Arabia and UAE have sought to optimize their energy resilience by boosting the capacity of existing alternative pipelines to the Strait of Hormuz. Will these countries be tempted to develop other alternative land routes in the future to protect themselves from threats to maritime routes ? Past and present experiences has shown that land corridors can also be highly exposed to geopolitical risks.

It is interesting to note that, when it comes to gas, the picture is somewhat different, as it is more balanced.However, land transport via pipelines, which still dominated before the Ukrainian crisis, is tending to be supplanted by maritime transport following liquefaction. The current ratio is now estimated to be around 55% for LNG compared with 45% for pipelines. The spectacular growth in gas production and trade since the start of the millennium and recent developments in gas transport mean that precise and reliable figures cannot be obtained in this instance, but there is a strong upward trend in the share of LNG, driven by the development of new liquefaction infrastructure and a demand for greater flexibility from the markets (particularly in Europe and Asia). The crisis in Ukraine and the closure of the European market to Russian gas (supplied mainly by pipeline) have accentuated this trend.

In the region under consideration, it is clear that the initial domination of the gas pipeline was exemplified in particular by Turkey’s survival strategy. At the end of the bipolar era, in order to clean up its cities, which were choked by smoke from coal-fired heating, and to support its economic development, the country decided to purchase gas on a massive scale from Russia. To secure its long-terme supply, it focused on pipeline infrastructures with the opening in 2003 of the Blue Stream gas pipeline, which crosses the Black Sea, before establishing itself as a key player in the Southern Gas Corridor to Europe. This initiative led to the commissioning of the Bakou-Tbilissi-Erzurum (BTE) gas pipeline in 2006, which partly followed the Bakou-Tbilissi-Ceyhan (BTC) oil pipeline, which had been inaugurated the previous year. Subsequently, establishing itself as a genuine gas hub, Turkey has invested in other major projects. From 2018, the TANAP (Trans Anatolian Natural Gas Pipeline), led by a Turkish-Azerbaijani consortium, has been transporting Caucasian gas to Europe via the Anatolian peninsula. Commissioned in 2020, the Turkish Stream, born of cooperation between Ankara and Moscow, exports Russian gas to Turkey and Europe, via Black Sea, bypassing Ukraine.

By contrast, in the wider gas market of the Eastern Mediterranean – from which Turkey is excluded – the choices regarding gas transit routes have been different and more favourable to LNG[2]. In 2010, Israel discovered the Leviathan gas field, whereas Cyprus identified several further north from 2011 onwards, and in 2015, Egypt confirmed the existence of huge gas reserves within its exclusive economic zone (notably the Zohr field)[3]. On 7 April 2026, the discovery of a new gas field containing 57 billion m3 and a condensate (light oil) deposit was announced by the Egyptian government and the Italian company ENI, which operates these energy resources. Over the past decade, this new source of revenue has enabled the revival of the liquefaction factory and terminals at Damietta and Idku, which had been operating at reduced capacity due to the depletion of Egypt’s older gas fields (in the Nile Delta, the Gulf of Suez or the Western desert).

Egypt, which also imports gas from Israel and Cyprus to liquefy and re-export it, has become a major LNG hub. A major consumer of gas for its domestic needs (domestic and industrial electricity…), it is looking towards Asian markets, which offer attractive opportunities, but it is also targeting the European market, which is seeking to diversify its supplies and represents a stable outlet. In June 2022, in this regard, it signed a major tripartite agreement with Israel and the European Union. This choice of LNG does not prevent Caireo from also taking interest in the EastMed subsea gas pipeline project that Cyprus, Israel and Greece launched in 2020 to connect the eastern Mediterranean to the southern shore of the European continent. The construction of this undersea pipeline is, however, hampered by significant costs and by the fact that its route crosses the exclusive economic zone demarcated by Libya and Turkey, to the west of the gas fields in the eastern mediterranean.

For the time being, we are therefore witnessing the emergence of two gas hubs in this region: one Turkish and the other Egyptian. The former is a transit hub, supplied mainly by Russian and Azerbaijani gas. Its LNG infrastructure remains limited (three regasification factories, used for import and re-export). The second is a hub that exports both its own gas and imported gas. For European markets, these two hubs are currently largely complementary, both contributing to the Old continent energy security . But they could become competitors, particularly with regard to onshore transport. Following the 2026 crisis, the construction of the Eastmed pipeline could lead to a direct connection between Eastern Mediterranean gas to Europe and the Qatar-Turkey gas pipeline project (Gulf-Turkey Gas Pipeline) could be revived, all the more so because the regime change in Damascus now makes it possible to cross Syria.

In any case, this leads us to conclude that the region has no shortage of gas and that the issue is more a question of determining the most cost-effective and the secure routes for exporting it to local and European markets. Until now, the choices made in this area have been fairly representative of the global distribution of gas transport, where pipelines have dominated and where LNG, although a minority, has attracted increasing interest from markets due to its flexibility. It remains to be seen, more generally, what the effects of the 2026 crisis will be on this situation, and, in particular, on the growth of LNG. The blockage of the Strait of Hormuz affected 20% of the global LNG flow, originating from Qatar (the world’s leading LNG producer), the UAE and Saudi Arabia. As with oil, it is likely that existing systems will be assessed in terms of their complementarity and the geopolitical constraint of the regions where they are deployed.

As a conclusion…

To conclude, we would like to summarise our observations on the impact of the crisis on oil and gas transport in the Middle-East.

As far as oil transport is concerned, it is clear that oil pipelines in the Middle-East do not serve as a complete substitute for sea routes, but that they are establishing themselves as an essential pillar of energy security. Their development reflects not so much a substitution as a strategic adaptation to an international environment marked by uncertainty. Analyses by international institutions also converge on this conclusion: oil pipelines are, above all, instruments of resilience, capable of mitigating the effects of a major crisis such as a closure of the Strait of Hormuz, without being able to entirely replace it.

As regards gas transport, pipelines have been little affected by the crisis and whilst the blockage of the Strait of Hormuz is likely to have short-term consequences for the development of maritime transport, it is thought to have little impacts on a global structural trend that favours LNG. The 2026 crisis could even accelerate investment in new liquefaction infrastructure on other continents, particularly in the vicinity of the Middle-East (West Africa).

In the longer term, these balances could be affected by changes in the global energy system. The expected decline in demand for hydrocarbons, the rise of renewable energies and the development of new forms of energy transport, notably hydrogen, are likely to reduce the importance of hydrocarbons. Nevertheless, in the year to come, their maritime transport routes and pipelines are expected to continue to profoundly shape the energy geopolitics of the Middle-East.

Notes

[1] Cf. BARR James, A line drawn in the sand, The Franco-British conflict that shaped the Middle East, Paris, Perrin, 2017, particularly chapter 12

[2] MARCOU Jean, La Turquie en Méditerranée orientale : entre revendications énergétiques et ambitions stratégiques, Diplomatie, N°105, septembre-octobre 2020, p. 53-57

[3] MOURAD Hicham, L’Égypte, nouveau hub énergétique régional », Diplomatie, N°105, septembre-octobre 2020, p. 61-65